%%{init: {'theme': 'default', 'themeVariables': {

'fontFamily': 'Inter, Segoe UI, Roboto, sans-serif',

'primaryColor': '#0d6efd',

'lineColor': '#6c757d'

}}}%%

flowchart TB

classDef reb fill:#ffe5e0,stroke:#ff6b6b,color:#7a1f1f,stroke-width:1.5px;

classDef nonreb fill:#e0f2ff,stroke:#0d6efd,color:#0b3d91,stroke-width:1.5px;

classDef pool fill:#eef2f7,stroke:#6c757d,color:#212529,stroke-width:2px;

X(("LSD Pool")):::pool

A["stETH<br/>(Rebasing)"]:::reb -->|"APY 3.8% / Comp 4/10"| X

B["mSOL<br/>(Rebasing)"]:::reb -->|"APY 6.2% / Comp 3/10"| X

C["rETH<br/>(Non-Rebasing)"]:::nonreb -->|"APY 3.5% / Comp 8/10"| X

D["cbETH<br/>(Non-Rebasing)"]:::nonreb -->|"APY 3.4% / Comp 9/10"| X

E["sfrxETH<br/>(Non-Rebasing)"]:::nonreb -->|"APY 4.6% / Comp 9/10"| X

linkStyle default stroke:#0d6efd,stroke-width:2px,opacity:0.95;

3 Market Background & Typology

Liquid Staking Derivatives (LSDs) have rapidly emerged as foundational assets across multiple blockchains, enabling capital efficiency, yield generation, and DeFi composability. Yet beneath the surface of this explosive growth lies a fragmented landscape marked by structural diversity, protocol asymmetries, and valuation opacity.

This chapter lays the groundwork for understanding the current LSD ecosystem. We begin with a panoramic view of protocol growth and cross-chain expansion. We then categorise LSDs by yield mechanism — rebasing vs non-rebasing — and dissect the implications for pricing and DeFi usage. A detailed comparison of major LSDs follows, highlighting trade-offs in yield, liquidity, and integration. Finally, we examine the systemic challenges facing the market: pricing inefficiencies, liquidity dispersion, and the absence of unified analytics.

Understanding these dynamics is essential for building LSDx — a credible, quantitative layer that enables rational allocation, risk measurement, and fair valuation across the LSD spectrum.

3.1 LSD Landscape: Growth, Chains, Protocols

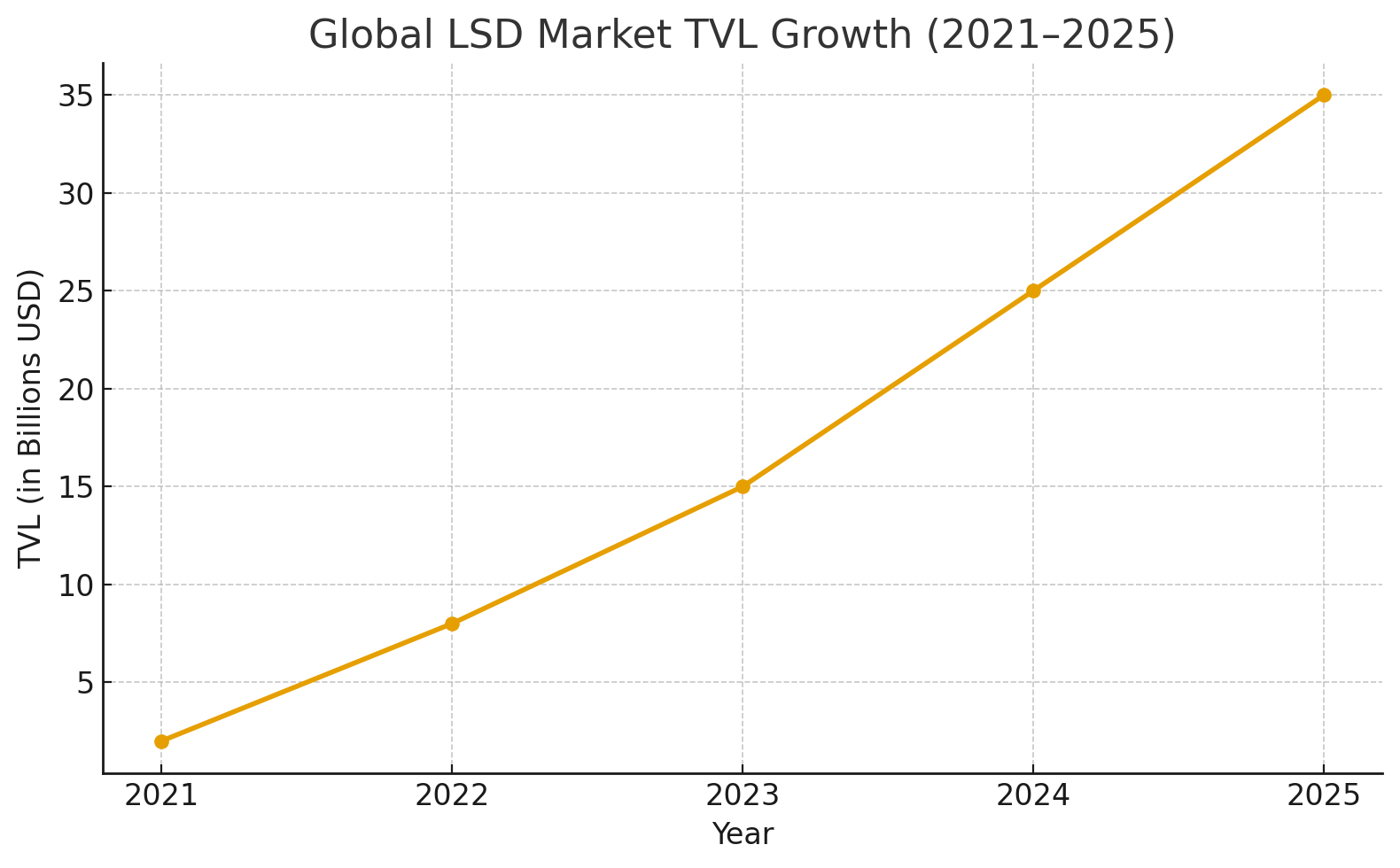

The Liquid Staking Derivatives (LSD) sector has rapidly evolved from a niche Ethereum staking workaround into a foundational layer of multi-chain DeFi infrastructure. As of mid-2025, LSDs collectively represent over $35 billion in Total Value Locked (TVL), with dozens of protocols offering tokenised staking products across Ethereum, Solana, Cosmos, and newer chains like Sui and Aptos.

This growth is driven by a structural shift in Proof-of-Stake economics. As staking becomes the dominant consensus mechanism, demand has grown for mechanisms that preserve both yield and liquidity — a gap that LSDs fill.

3.1.1 Market Segmentation: LSD Types by Chain

| Chain | LSD Protocols | Native Token | LSD Example | Notes |

|---|---|---|---|---|

| Ethereum | Lido, Rocket Pool, Coinbase, Frax | ETH | stETH, rETH | Most mature and liquid LSD ecosystem |

| Solana | Marinade, Jito, Lido | SOL | mSOL, jitoSOL | High APYs, but fragile DeFi integrations |

| Cosmos | Stride, pSTAKE, Quicksilver | ATOM, OSMO, etc. | stATOM, stkOSMO | Interchain LSD support growing |

| Avalanche | Benqi | AVAX | sAVAX | Limited DeFi usage so far |

| Polygon | Stader, ClayStack | MATIC | stMATIC | Used in rollup-native strategies |

| Sui / Aptos | Various experimental LSDs | SUI, APT | – | Early-stage protocols in development |

LSDs are no longer just an Ethereum-native phenomenon. Cross-chain expansion has led to fragmented liquidity, inconsistent token standards, and diverse validator reward dynamics — all of which complicate yield comparisons and risk evaluation.

3.1.2 Growth Trends: TVL, Adoption, and Yield Compression

- TVL Expansion: LSD TVL has grown from ~$2B in 2021 to over $35B by 2025.

- Validator Pooling: Protocols now support permissionless node operators (e.g. Rocket Pool), creating decentralised alternatives to centralised staking.

- Yield Compression: As staking becomes crowded, base yields decline — creating more pressure to optimise risk-adjusted return.

In parallel, LSDs have begun to influence:

- Stablecoin collateral frameworks

- Structured products (delta-neutral vaults, tranching)

- Cross-chain bridges (e.g., stETH as wrapped collateral)

- Index products (LSD baskets, ETH rebalancing funds)

3.1.3 Protocol Differentiation

| Protocol | Key Feature | APY Range | Peg Mechanism |

|---|---|---|---|

| Lido (stETH) | Largest; liquid; rebasing | 3.5–4.2% | Curve pool + DAO |

| Rocket Pool | Permissionless nodes; insurance pool | 3.0–4.0% | rETH premium model |

| Coinbase cbETH | Centralised custody | ~3.5% | Floating price |

| Frax ETH | Dual-token model (frxETH + sfrxETH) | 4.0–4.8% | Liquidity layer + vault |

| Jito (Solana) | MEV-boosted staking rewards | 6.0–7.5% | Native SOL wrapping |

| Stride (Cosmos) | Multichain Cosmos staking aggregator | Varies | Interchain accounts |

These protocol differences matter. Peg mechanics, validator incentives, slashing protections, and token design all impact the true yield, price trajectory, and risk profile of each LSD.

3.1.4 Implications for Analytics

The LSD space is heterogeneous by design. It mixes:

- Native chain mechanics (Ethereum vs Solana vs Cosmos)

- Validator economics

- Token rebasing logic

- Exit queue constraints

This diversity makes cross-protocol comparison nearly impossible without a unifying analytical layer — a gap that LSDx is designed to fill.

LSDx’s mission begins with this complexity:

To turn a fragmented, protocol-specific landscape into a structured, quantifiable ecosystem. — Vahab Rostampour

3.2 Typology: Rebasing vs Non-Rebasing LSDs

Liquid Staking Derivatives (LSDs) are not a monolith. One of the most fundamental distinctions in LSD design is between rebasing and non-rebasing mechanisms. This typology directly impacts how rewards are distributed, how token prices behave, and how LSDs integrate with other DeFi protocols.

3.2.1 Rebasing LSDs

Rebasing LSDs deliver staking rewards by increasing the holder’s token balance over time. The token price remains relatively fixed (typically close to 1:1 with the native staked asset), but the quantity of tokens in the user’s wallet grows daily or per epoch.

3.2.1.1 Mechanism & Examples

- Daily or epoch-based rebase adjusts token balances upwards

- Smart contract emits “rebase” to update balances

- Balance increases per epoch (e.g., 1 → 1.0001 → …)

- Token price remains ~constant (usually pegged e.g., 1 stETH ≈ 1 ETH)

- Examples: stETH (Lido), mSOL (Marinade), ankrETH (Ankr)

3.2.1.2 Advantages

- Intuitive for users: your balance grows

- Peg remains stable—rebase compounding is transparent

- Simpler accounting for wallets and DeFi tooling

3.2.1.3 Limitations

- Not easily compatible with some DeFi protocols (e.g., LPs, vaults)

- Hidden value accumulation—price charts alone are misleading

- May not integrate seamlessly with DeFi primitives requiring fixed token balances

3.2.2 Non-Rebasing LSDs

Non-rebasing LSDs deliver staking rewards via token price appreciation. The user’s balance stays constant, but the value of each token increases over time as staking rewards are compounded into the price.

3.2.2.1 Mechanism & Examples:

- No change in token quantity; balance stays constant; value comes from price increase

- Token price increases gradually

- Accrual is continuous and observable in price chart

- Examples: rETH (Rocket Pool), cbETH (Coinbase), sfrxETH (Frax)

3.2.2.2 Advantages:

- Fully compatible with DeFi protocols (fixed units), vaults, LP positions

- Ideal for integrations in structured products, derivatives, and LPs where fixed token quantity matters (e.g. options, bonds)

- More transparent reward accumulation via price chart

3.2.2.3 Limitations:

- Price deviates from native token, introducing depeg risk (e.g., cbETH ≠ 1 ETH)

- Users must rely on price charts to see yield, which may be noisy

- Potential UX confusion around value representation

- Peg deviation risk under market stress

3.2.3 Analytics Implication

This typology is not cosmetic — it impacts everything from valuation logic, risk metrics, to composability in broader DeFi.

LSDx explicitly accounts for this in its architecture:

| Feature | Rebasing LSDs | Non-Rebasing LSDs |

|---|---|---|

| Valuation Method | Balance tracking | Price-based NPV |

| Peg Measurement | Token quantity ↔︎ ETH | Price deviation ↔︎ ETH |

| Reward Integration | Rebase % / day | Price gradient |

| Risk Metrics Compatibility | Limited (due to rebases) | Full DeFi support |

Understanding whether an LSD is rebasing or not is the first step to correctly valuing, scoring, or integrating it.

This is why LSDx includes this classification as a primary model input.

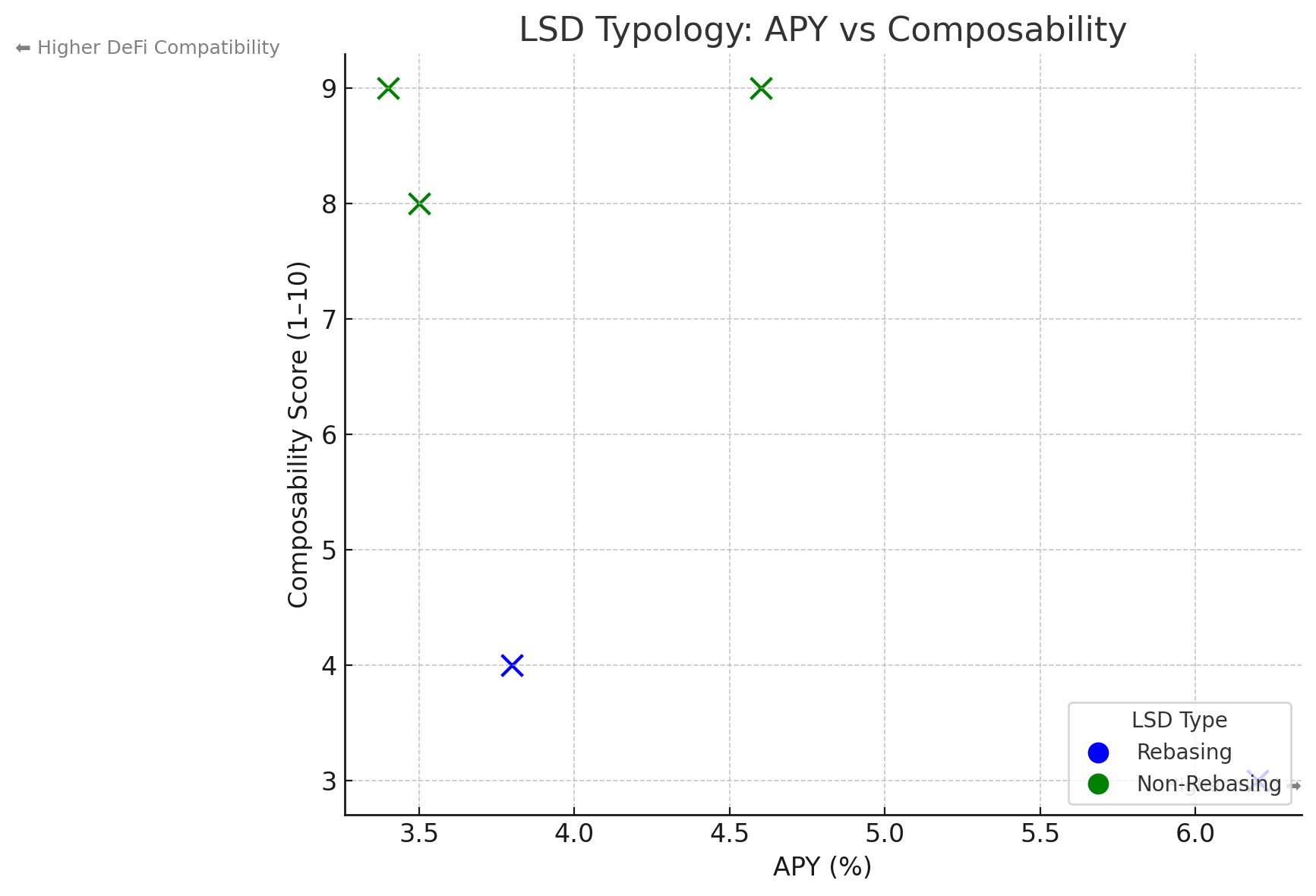

3.2.4 Visual Insight: APY vs Composability

This chart captures how:

- Rebasing LSDs often deliver similar or higher APYs, but are less composable.

- Non-rebasing LSDs offer greater integration flexibility in DeFi.

3.2.5 Exit Delays & Queue Risk

Understanding LSD typology is incomplete without considering unbonding or exit delays:

Ethereum’s exit queue, as of August 2025, measured between 17–18 days in withdrawal delay

Source: CryptoSlate,

Source: AInvestThis introduces liquidity bottlenecks, especially during market stress.

Rocket Pool’s rETH users also experience similar delays due to validator queue and processing limits

Source: Fluidkey,

Source: Reddit

These delays affect:

- Fair value modeling (e.g., NPV haircut for redemption latency)

- Risk scoring (liquidity risk premium)

- Smart contract logic (e.g., accounting for delayed redeemability)

3.2.6 Analytics Implications

| Feature | Rebasing LSDs | Non-Rebasing LSDs |

|---|---|---|

| Valuation Method | Balance accrual logic | Price appreciation logic |

| Peg Tracking | Stable, linked to native | Requires spread modeling |

| Integration in DeFi | Limited composability | High composability |

| Exit Risk | Hidden in balance changes | Price-visible queue effects |

In summary, this typology is a primary driver of how LSDx models value, risk, and integration behaviour. Correctly classifying LSDs ensures accurate analytics outputs — from fair value to yield risk ratios.

3.3 Comparison of Major LSDs

A clear understanding of leading Liquid Staking Derivatives (LSDs) across chains is essential. Each protocol implements unique design, governance, and reward mechanisms — all of which inform valuation, risk, and composability.

3.3.1 Protocol Overview Table

| Protocol | Type | Native Chain | Yield Mechanism | Approx. APY (2025) | Fee Structure | Key Differentiator |

|---|---|---|---|---|---|---|

| Lido (stETH) | Rebasing | Ethereum | Balance increase | ~3.5–4.0% | ~10% of staking rewards | Largest TVL (~30% of ETH staking) :contentReferenceoaicite:0 |

| Rocket Pool (rETH) | Non‑rebasing | Ethereum | Price appreciation | ~3.5% | ~14% + node operator cut | Permissionless nodes, decentralised approach :contentReferenceoaicite:1 |

| Coinbase (cbETH) | Non‑rebasing | Ethereum | Price appreciation | ~3.4% | ~35% of staking rewards | High retail accessibility; centralized :contentReferenceoaicite:2 |

| Frax (sfrxETH) | Non‑rebasing | Ethereum | Price appreciation | ~4.0–4.8% | Protocol-based fees | DeFi-native vault abstraction |

| JitoSOL | Rebasing | Solana | Balance increase | ~6.0–7.5% | ~4% + withdrawal fee | MEV-enhanced yield; Solana-native :contentReferenceoaicite:3 |

| Marinade (mSOL) | Rebasing | Solana | Balance increase | Moderate | Variable | Long-standing Solana LSD |

3.3.2 Analytical Highlights

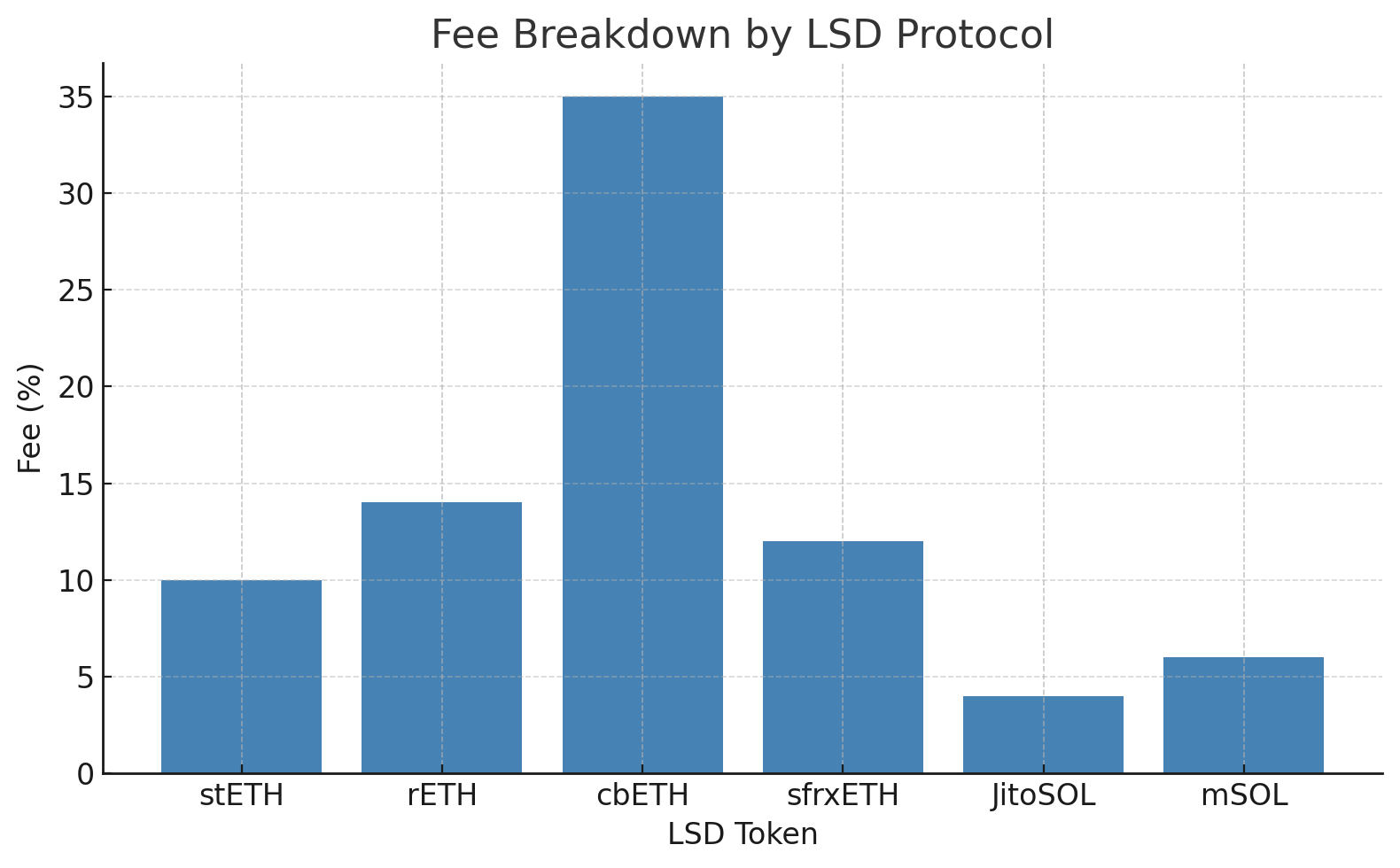

3.3.2.2 Fee Impact on Yield

- Across protocols, fee structures vary: e.g., Lido charges ~10%, Rocket Pool ~14% + operator cut, and Coinbase charges ~35% :contentReferenceoaicite:5.

- These fee differences account for significant yield dispersion, even when raw staking rewards are similar.

3.3.2.3 Composability & Integration

- Non-rebasing LSDs (rETH, cbETH, sfrxETH) offer superior DeFi compatibility due to fixed token balances.

- Rebasing LSDs (stETH, JitoSOL) require wrapped versions (e.g., wstETH) for integration across LPs and vault systems :contentReferenceoaicite:6.

3.3.2.4 Token Behavior & Peg Stability

- stETH trades closely to 1:1 with ETH but may occasionally deviate slightly on DEXs due to liquidity or demand cycles :contentReferenceoaicite:7.

- cbETH and rETH show more permanent price premiums or discounts, depending on market demand and redemption friction :contentReferenceoaicite:8.

3.3.3 Implications for Analytics

Each LSD carries unique characteristics that LSDx must account for:

- Value Modeling: Rebasing vs non‑rebasing changes yield recognition — balance growth vs price appreciation.

- Peg Risk: Rebasing systems rely on peg maintenance; non-rebasing LSDs need price spread tracking.

- Composability Needs: Rebasing LSDs may require wrapping strategies for vault integration.

- Fee & Reward Structures: Fee models influence effective yield and should factor into “fair value” calculations.

This figure shows fee breakdown by LSD protocol. It visualizes how much each protocol charges in staking or validator fees. Notably:

- Coinbase’s cbETH takes a significant cut (~35%)

- JitoSOL and mSOL offer lower fees

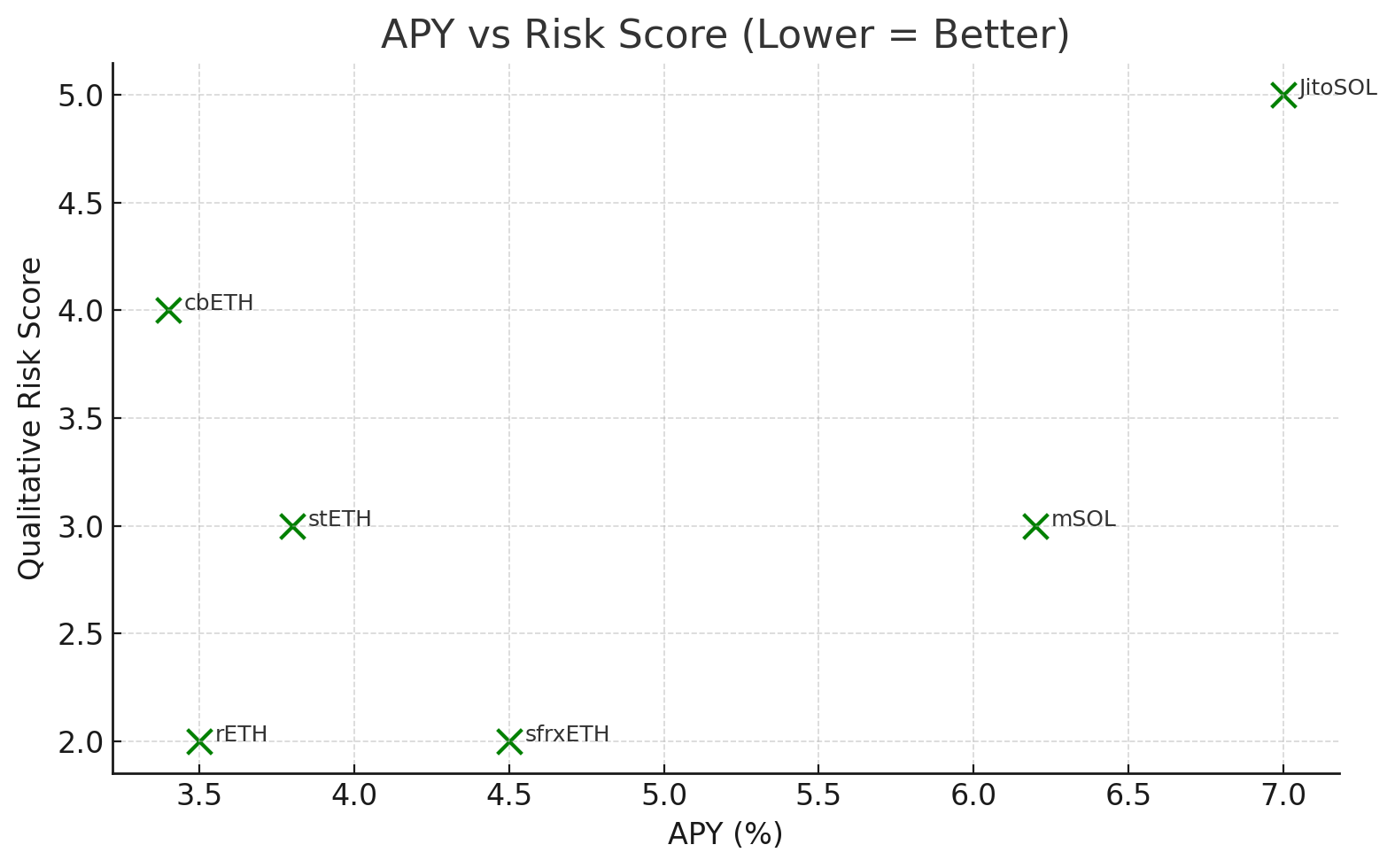

This figure shows APY vs qualitative Risk score. It shows the trade-off between expected yield and qualitative risk.

- JitoSOL offers the highest APY but with higher risk

- sfrxETH appears optimal with relatively high APY and low risk

All together, these protocol-level nuances reinforce the need for a unified analytical layer — one that normalizes metrics and meshes valuation, risk, and integration across the LSD spectrum.

3.4 Market Fragmentation and Challenges

Despite their explosive growth and adoption, Liquid Staking Derivatives (LSDs) suffer from substantial market fragmentation. There is no unified marketplace, pricing oracle, or standard analytics layer — leading to inefficiencies and risk blind spots across users, protocols, and allocators.

3.4.1 1. Pricing Inconsistency Across LSDs

LSD tokens like stETH, rETH, and cbETH may all represent staked ETH, but their prices deviate due to:

- Rebasing vs non-rebasing mechanisms

- Secondary market liquidity and slippage

- Withdrawal queue effects and delays

- Trust in issuers and perceived risk (e.g., slashing exposure)

For example, stETH typically trades within ~0.2% of ETH, while cbETH often has a persistent discount or premium depending on market conditions.

The lack of a standard fair value model makes it difficult to evaluate which LSD is underpriced or offers better risk-adjusted returns.

3.4.2 2. Liquidity Fragmentation

Liquidity is scattered across: - Native protocol liquidity pools (e.g., Curve stETH/ETH, Uniswap cbETH/ETH) - Centralised exchanges (e.g., Coinbase, Binance) - Cross-chain bridges and wrapped LSDs

This causes: - Inefficient routing of swaps - Price spreads between venues - Depeg events under stress

During volatility, LSDs like mSOL or JitoSOL have traded at 2–6% discounts on Solana DEXs due to liquidity imbalances and withdrawal constraints.

3.4.3 3. Risk Transparency Gaps

Users often have no clear view of: - Validator performance or slashing track record - Exit queue length or expected unlock delay - Protocol-level governance centralisation

There is no standardised risk score, leaving institutions and retail users vulnerable to hidden tail risks.

3.4.4 4. Composability Gaps

Many DeFi vaults, money markets, and structured products: - Do not support rebasing tokens natively (e.g., stETH) - Require wrapped versions (e.g., wstETH), introducing complexity - Lack consistent collateral treatment across LSDs

This impairs the ability of users to deploy LSDs as collateral efficiently, reducing capital velocity.

3.4.5 5. Lack of Yield Comparability

Due to differing: - Fee structures (e.g., Lido vs Rocket Pool) - Reward schedules - Block-level vs epoch-level updates

… there is no universal way to compare APY across LSDs on a net basis.

Protocols often report gross yield, not accounting for validator slashing, downtime, or platform fees — misleading users and institutions.

3.4.6 Summary Table: Fragmentation Challenges

| Domain | Challenge Example | Resulting Pain Point |

|---|---|---|

| Pricing | stETH vs cbETH spread changes daily | Fair value unclear |

| Liquidity | mSOL depegging on Solana DEXs | Exit risk under stress |

| Risk Transparency | Unknown validator slashing metrics | Poor risk-adjusted allocation |

| Composability | wstETH needed for integration | UX and collateral friction |

| Yield Metrics | No net APY standard | Inconsistent performance reporting |

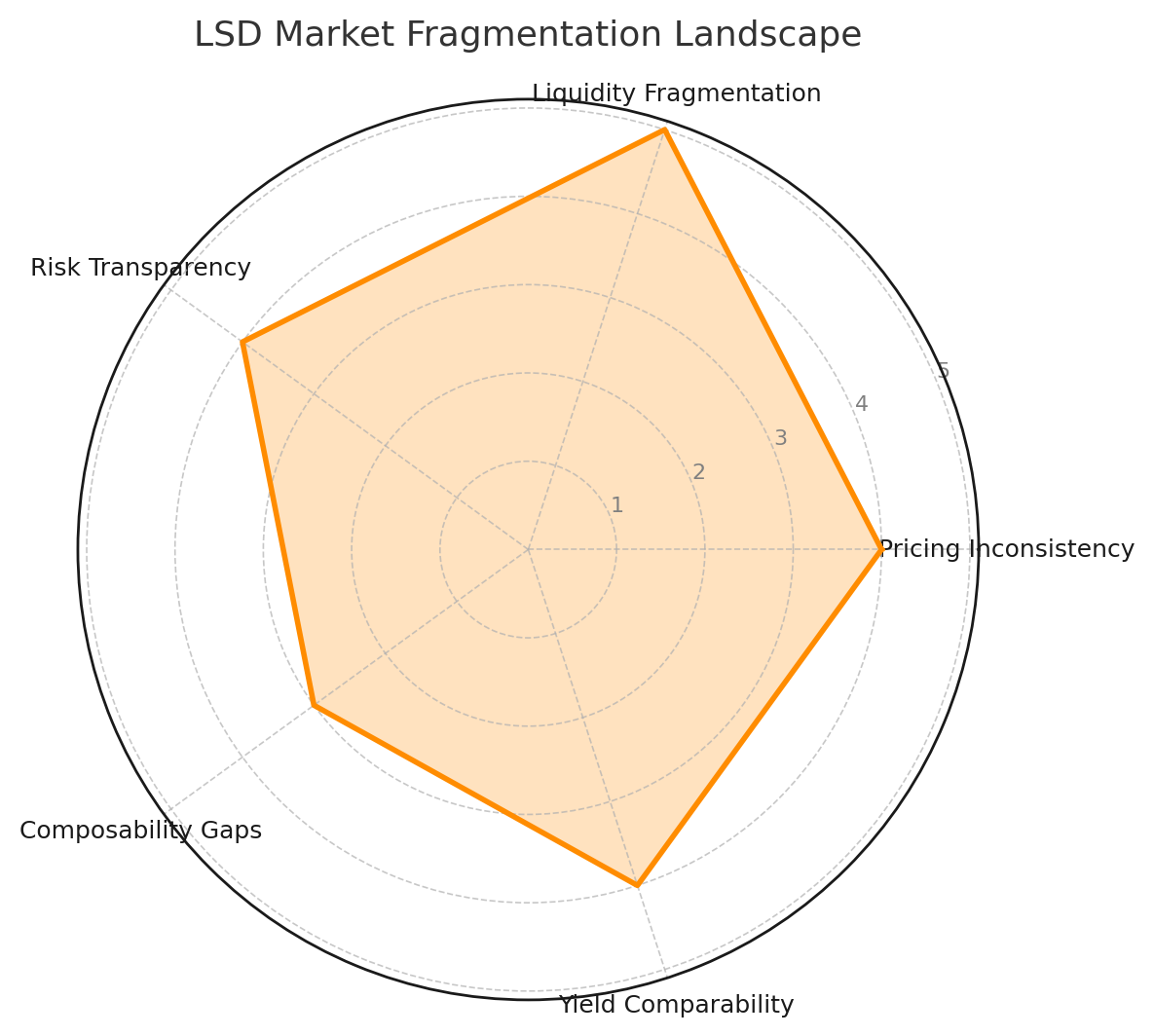

Thsi figure is the LSD Market Fragmentation Landscape radar chart. It visually maps key pain points in the current LSD ecosystem:

- Liquidity fragmentation scores the highest (5/5)

- Composability is less severe but still impactful (3/5)

- All other categories show moderate-to-high fragmentation

3.4.7 Strategic Insight

To unlock the full potential of LSDs, the market needs:

- Normalised valuation frameworks

- Cross-token risk scoring

- Smart contract access to fair pricing

- Transparent APY comparison dashboards

- Liquidity-aware portfolio tools

This is the core thesis behind the LSDx analytics layer.